Human is deemed to commit errors. Yet learning from them and not repeating them is something we tend to practice. In Accounting we need to detect errors and correct them. Let’s increase our Financial Quotient “FQ” by learning easy ways to find these types of accounting & bookkeeping errors & learn how to avoid them.

There are certain accounting & bookkeeping errors that you may easily detect while preparing a Trial Balance. For example, balancing error, posting error (posting of a wrong amount or on the wrong side of an account). These errors get rectified at the time of preparation of Trial Balance.

There are certain errors that go undetected while preparing Trial Balance. You need to detect such errors and rectify them before preparing financial statements.

Table of Contents

Accounting & bookkeeping errors can be detected & corrected at the following stages:

- Stage I: Before preparation of Trial Balance

- Stage II: After preparation of Trial Balance but before preparing the final accounts (i.e., financial statements)

Above are the 2 stages that help to detect the accounting & bookkeeping errors and rectify them.

Stage I Errors

Ledger balances are not drawn and hence accounts are not yet closed.

There are two kinds of Stage I errors:

- Errors for whose rectification no journal entry is possible (e.g., sales account is undercast by Rs.20,000)

- Errors which can be rectified with the help of a journal entry.

Example 1: Goods returned by a customer, Mr. X, worth Rs. 5,650 has been posted in the Return Inward Account as Rs.5,560 and in Mr. X Account as Rs.6,550

In this case, the correct entry should have been:

Return Inward Account Debit Rs.5,650

X Account Credit Rs.5,650

Hence, the Return Inward Account is debited less by Rs.90 (5650-5560) and X Account is credited more by Rs.900 (6550-5650).

Rectification entries would therefore be:

Return Inward Account Debit Rs.90

X Account Debit Rs.900

Since both entries are on the debit side of the affected accounts, no journal entry is required to be passed. Instead necessary rectifications are to be carried out in the respective accounts directly.

Example 2: Salary paid Rs.6000 has been posted to Rent Account.

- Rent Account is debited excess by Rs.6,000 and Salary Account is debited less by the same amount.

Hence, the rectification entry will be:

Salary Account Debit Rs.6,000

Rent Account Credit Rs.6,000

The above rectification is possible with the help of a complete journal entry.

Stage II Errors

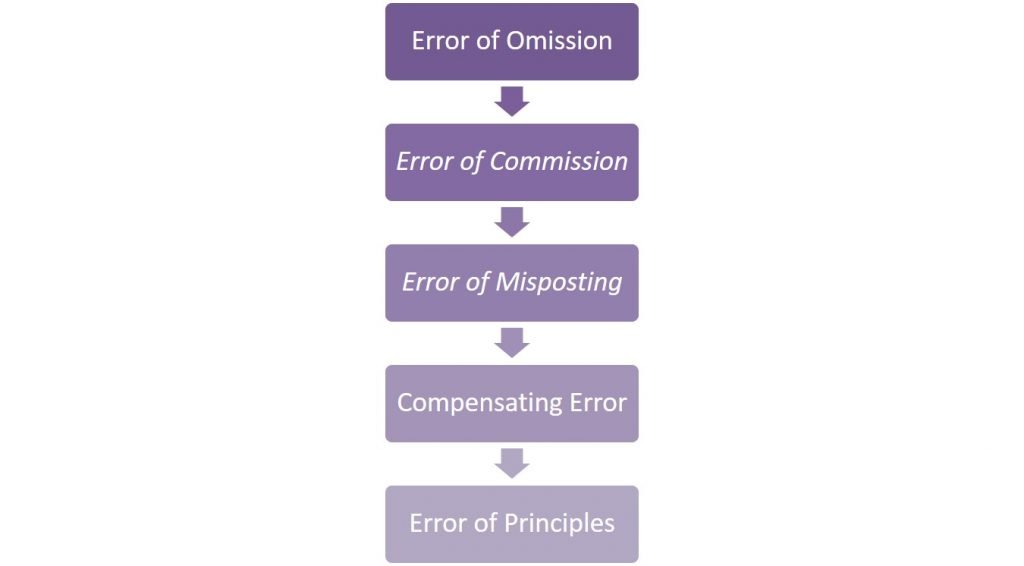

- Compensating errors, errors of commission, errors of omission, errors of misposting, and errors of (accounting) principles.

- Since the Trial Balance is already prepared, ledger balances are drawn.

- Hence, such errors can only be rectified with journal entries.

Example 1– (Error of Omission): Bank charges of Rs.150 are not recorded in the books of accounts.

- This is an error of omission as the transaction has not at all been recorded in the Primary Books.

- Following ground accounting rules, the rectification entry will be:

Bank Charges Account Debit Rs.150

Bank Account Credit Rs.150

Example 2– (Error of Commission): Cash of Rs.10,000 received from Mr. X wrongly recorded as Rs.1000.

- This is called an error of commission where an amount is wrongly entered. (but in correct side of the account).

- Rectification entry:

Cash Account Debit Rs.9,000

X Account Credit Rs.9,000

Example 3– (Error of Misposting): Cash of Rs.10,000 received from Mr. X wrongly posted to Mr. Y Account.

- This is called an error of misposting where an amount is wrongly entered in another account

- Rectification entry:

Y Account Debit Rs.10,000

X Account Credit Rs.10,000

Example 4-(Compensating Error): Interest expenses of Rs.1,000 were wrongly posted as Rs.100 and cash sales of Rs.2,100 were wrongly posted to Sales Account as Rs.1,200. You can observe that the effect of one error (interest expenses debited less by Rs.900) was compensated by another error( sales account credited less by Rs.900). One error compensates for the other error in such a way that Trial Balance still tallies.

- Rectification entry:

Interest Expenses Account Debit Rs.900

Sales Account Credit Rs.900

Example 5– (Error of Principles): Travelling expenses of Rs.12,000 incurred in connection with the purchase of heavy equipment were debited to the Travelling Expenses Account.

- Accounting principles recommend that expenses incurred in connection with the construction/purchase of an asset can be added to the cost of the asset till the asset is ready for use. Hence, this is an error of accounting principles.

- Rectification entry

Equipment Account Debit Rs.12,000

Travelling Expenses Account Credit Rs.12,000

Let us know your thoughts on how to Detect such Errors?

Funfact:

A company might have to pay heavy penalties if errors occur in its financial statements. As it leads to misrepresentation of facts. In 2019, the Securities and Exchange Commission asked Hertz to pay $16 million in penalties due to multiple misstatements of material facts in its financials. Hertz did pay the penalty.